Mortgage Fixed vs Floating in NZ (2026): The Real Trade-off

Fixed locks your rate, floating moves with the OCR. In a falling-rate environment like 2026, which makes more sense? A practical guide to splitting, breaking, and the small print Kiwis miss.

Steady connects your bank and tracks it all automatically — no spreadsheets. Join the waitlist for early access.

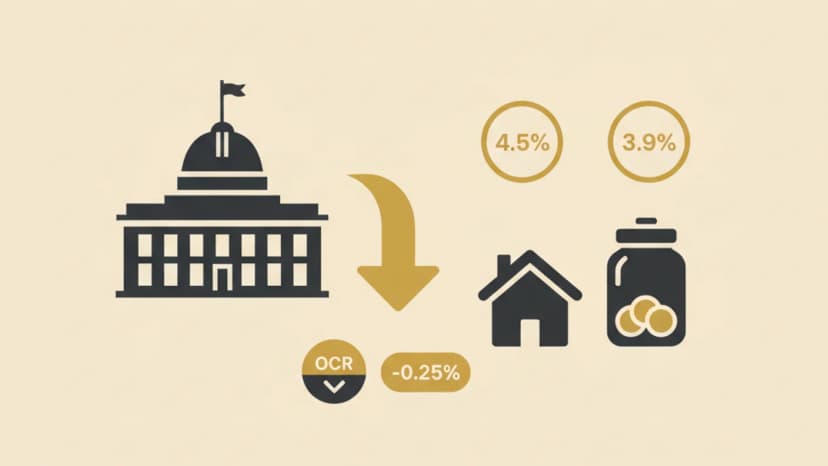

The Reserve Bank of New Zealand cut the OCR three times between November 2025 and May 2026, dropping it from 5.25% to 3.25%. Floating mortgage rates followed — most banks now sit around 6.00% floating vs 5.95–5.99% on a 1-year fixed.

That tiny gap is the whole question: lock in for certainty, or stay floating and ride further cuts down?

How they actually work

Fixed: You agree a rate for a set term (6 months to 5 years). The payment doesn't move. If rates fall, you don't benefit. If rates rise, you're insulated. Breaking a fixed rate early triggers a break fee that can run into thousands.

Floating: Rate moves with the bank's floating reference rate, which tracks the OCR loosely. You can repay extra any time, swap to fixed any time, and there's no break fee.

The 2026 case for floating

Most NZ economists expect 1-2 more OCR cuts in 2026 (taking it to ~2.75%). If you float, your rate likely drops another 0.25-0.50% over the next 9 months.

Floating downsides:

- You pay ~0.05% more today than the 1-year fixed.

- The bank can lift the floating rate at any time without warning.

- Your payment changes every cut — annoying for budget tracking.

The 2026 case for fixing (short)

A 6-month or 1-year fix lets you lock today's rate while keeping near-term optionality. If rates fall, you re-fix lower in 6-12 months. If they rise (unlikely but possible), you're protected.

Most NZ mortgage brokers in 2026 are recommending 6-month or 1-year fixed over longer terms — the curve says short.

Don't fix long (2-5 years) right now

Locking in 3-5 years at ~6% in a falling-rate environment is the worst of both worlds: you pay above market, and you can't get out without a five-figure break fee.

The split-loan trick

Most NZ banks will split your mortgage into multiple tranches — say 60% on a 1-year fixed at 5.95% and 40% floating at 6.00%. This means:

- Most of your payment is stable.

- A meaningful chunk benefits from future OCR cuts.

- You can pay extra on the floating slice without break fees.

For a $500k mortgage, this is the default move for most Kiwis right now.

Break fees: read this before you fix

If you fix and then need to break (selling the house, refinancing, lump-sum repayment), the bank charges the lost interest they would have earned vs current rates.

In a falling-rate market, break fees get LARGE — because the gap between your fixed rate and the current rate widens. A $500k loan fixed at 5.95% with 2 years to run, broken when rates have dropped to 4.50%, can cost $12,000+.

Rule of thumb: if there's any chance you'll sell or refinance, keep at least 30% floating.

What Steady can do

Once your mortgage is set up, log it as a Liability in Steady. You'll see:

- Monthly interest cost line-itemed in your spending.

- Forecasts that include the next rate-change date.

- Goal-progress tracking if you're paying down extra.

Disclaimer: This is general education, not personalised financial advice. Run any specific scenario past a licensed Financial Advice Provider before signing.

Steady tip: Track every rate-change letter your bank sends — over a 30-year mortgage the small movements compound to tens of thousands. A 0.25% saved on $500k = $1,250/year forever.

Written by Sam Wilson

Founder, Steady

Sam is a New Zealand founder building Steady — a personal finance app designed for Kiwis, integrated with every major NZ bank via Akahu. He writes about money, bank integrations, and what actually works for everyday New Zealanders.More about Sam

Steady connects your bank and tracks it all automatically — no spreadsheets. Join the waitlist for early access.

Suggested reads

More from the Steady blog

OCR Cuts in 2026: What They Mean for Your Mortgage and Savings

The Reserve Bank dropped the OCR to 3.25% in early 2026, with another cut likely. Here's exactly what that does to your mortgage repayments, your savings interest, and what to do about both.

ANZ vs ASB vs Kiwibank: Which Is the Best NZ Bank in 2026?

A head-to-head comparison of New Zealand's three big retail banks for everyday accounts, savings rates, mobile apps, and fees in 2026.

How to Save for Your First Home in NZ (2026 Guide)

NZ house deposit in 2026: you need $120k (or less with these tricks). KiwiSaver withdrawal, First Home Grant, and the exact savings plan.

Ready to sort your money?

Steady connects to your NZ bank accounts and helps you track spending, set goals, and get AI-powered insights.

Try Steady free